We are testing the uncovered interest rate parity (UIRP) hypothesis on USD/MXN (market convention: MXN per 1 USD). The theory predicts that the expected exchange rate move should offset the interest rate differential. In practice, this means that carry should not deliver persistent excess returns. We launched a spot demo experiment and added a twist to the rules. We opportunistically took even small profits and re‑entered positions when we deemed it appropriate. In this article, we show where the theory fits the data and where real‑world dynamics and risk regimes flip the script.

Uncovered Interest Rate Parity on a Napkin

When one country’s short-term interest rate is higher than another’s, UIRP says the exchange rate is expected to move against the higher-yielding currency by roughly that interest gap. Put simply: the extra interest is “paid back” by an expected currency move. So an unhedged carry trade shouldn’t deliver free, persistent excess returns on average.

If Mexico’s short rate sits a few percentage points above the U.S.’, the peso would be expected to lose roughly that amount against the dollar over the same period, offsetting the extra interest. The time horizon for this relationship is generally considered to be the long run.

The offset often doesn’t arrive on schedule. In calm, yield-seeking markets, carry can show steady gains; in stressed markets, those gains can be given back quickly. This mismatch between theory and observed returns is the well-known forward premium puzzle.

Why Did We Chose USD/MXN for Our Forex Carry Trade?

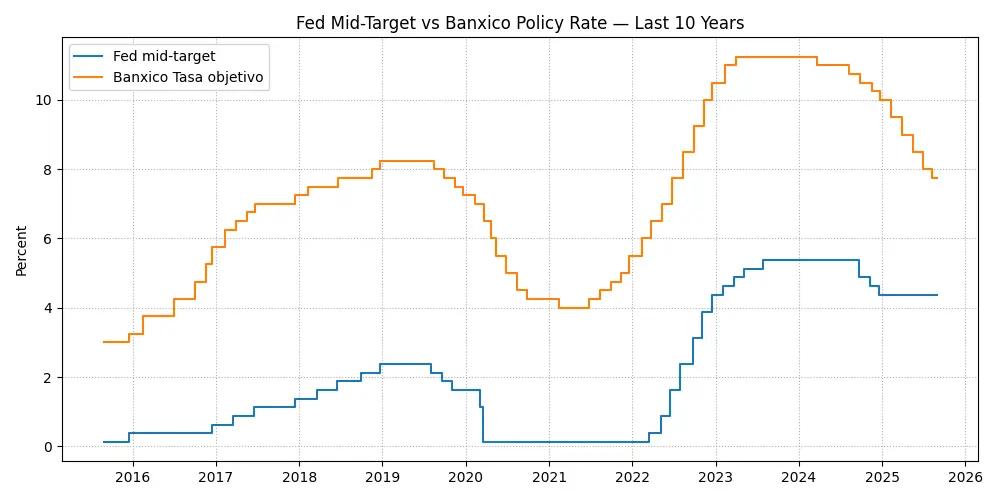

High‑yielding emerging market (EM) currency (MXN) versus low‑yielding (USD). This is a classic setup for testing UIRP and discussing carry trades (we will add a chart of the interest rate differential between the United States and Mexico below). To be precise, we traded other EM currencies as well (USD/ZAR, USD/TRY), but the absolute majority of trades was in USD/MXN.

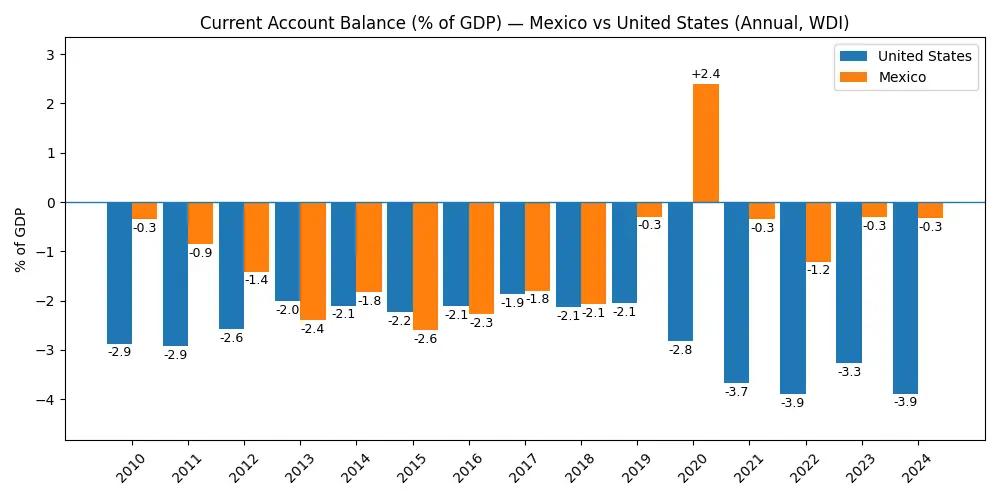

The pair is liquid enough for practical tests and has a rich history of market regimes (risk‑on/off), which is essential for seeing when carry “pays” and when it “punishes.” We also track two additional macro metrics: the current account balance (surplus/deficit) and foreign direct investment (FDI) into Mexico.

The current account tracks net flows of goods and services, cross-border income (interest, dividends, wages), and transfers such as remittances, usually shown in USD or as a share of GDP. A surplus or a narrowing deficit means a smaller external financing need and steadier natural demand for MXN, which is generally supportive for the currency (in the long-run).

Foreign direct investment (FDI) records long-term cross-border investment that conveys control or lasting interest (typically ≳10% equity), including new plants, reinvested earnings, and intra-group loans. Persistent, broad-based FDI inflows signal confidence in Mexico’s productive capacity and bring relatively “sticky” (“sticky” is econ-speak for “slow to adjust” or “linger”) capital tied to real activity. These dynamics tend to support MXN over multi-quarter horizons.

Efficient Markets Angle

The efficient markets hypothesis (EMH) points the same way. The more informationally efficient a market is, the faster new data are priced into assets and the shorter-lived any informational edge. Developed markets typically have deeper liquidity and stronger institutions, so mispricings are competed away quickly. Emerging markets can have slower information diffusion and higher frictions. As a result, apparent anomalies show up more often—but usually alongside higher crash risk and trading costs.

Nuance: In FX, persistent carry returns are often interpreted less as “inefficiency” and more as compensation for risk (liquidity/volatility/regime risk), not a free lunch.

Our Experiment Design

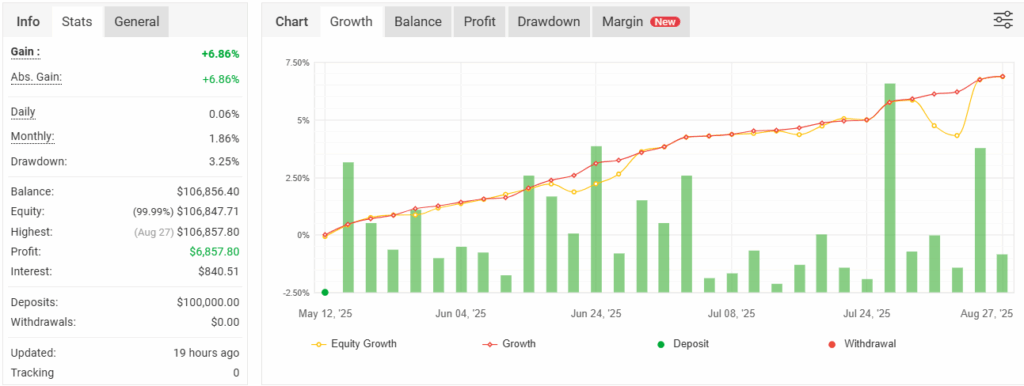

We observed the strategy for several months on a spot demo account. The experiment started in early May 2025, and it is still running as of the date of this article. We acknowledge this is a short window for definitive conclusions, but the results already merit attention.

Starting Balance and Other Account Parameters

- Initial balance: 100,000 USD.

- Leverage: 1:100.

- Broker: FxPro (we are not affiliated with them)

Trade Implementation

The core idea is a classic unhedged carry. We buy MXN (sell USD/MXN) as the high‑yielding currency versus USD and hold to collect swap.

We deliberately did not follow the canonical “hold long carry positions for months with high leverage” approach. Moreover, we added an opportunistic position‑management rule.

We close the position on positive P&L (no minimum threshold), then reopen when we judge the moment appropriate (based on discrete signals from micro‑dynamics to rate events).

This departs from “pure” UIRP (which assumes a passive exposure over a horizon comparable to the rate tenor), but in practice it reduces time in the market and helps sit out local USD spikes.

Costs

We account for spread, rollover (swap), and trading commissions. Demo accounts, by design, simulate trading without real money, which eliminates the real-world liquidity and price volatility that cause slippage in live accounts. However, given the nature of carry trades, slippage is non-trivial for small-target strategies. That’s why we avoid low-liquidity windows.

Evaluation Metrics

Because this is an ongoing experiment, the current account status and equity curve will be shown on the chart below and on Myfxbook.

What This Twist Adds to Uncovered Interest Rate Parity?

- Pros: trims some tail risk of long holding by reducing time in the market.

- Cons: forfeits part of the carry and can knock out of trends via a series of small takes; transaction load rises. At the end of the day, it was a conscious trade‑off.

- For an EM carry, managing regimes (monetary policy changes, volatility, global flows, oil) matters as much as the rate differential itself.

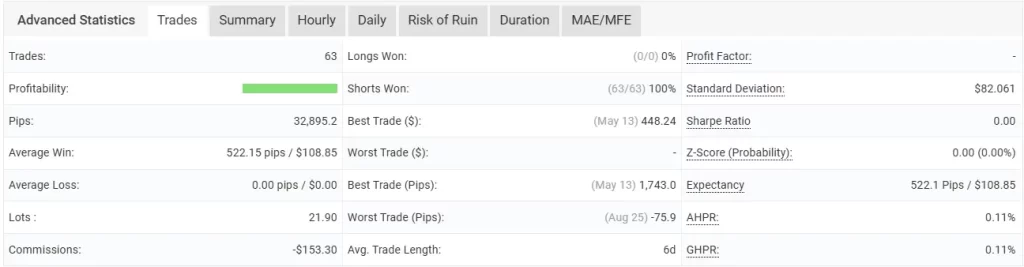

Preliminary Results of Our UIRP Based Carry Trade

We do realize that our sample size is relatively small; nevertheless, we felt that we should share our results.

Risks of a Forex Carry Trade (USD/MXN)

Carry trades tend to pay slowly and lose quickly. The return distribution is negative-skewed with fat tails—long stretches of small, steady gains punctuated by sharp drawdowns.

Regime flips (risk-on → risk-off). In risk-on environments, investors reach for yield. Emerging market currencies such as MXN can benefit. In risk-off, capital rotates to safety (USD/Treasuries) and MXN sells off, so months of carry may unwind in days. Regime tone is often monitored via VIX/MOVE, DXY, EMBI, and S&P 500 futures. Mitigation practices in the literature include volatility-scaled position sizing, rules that taper gross exposure when realized or implied volatility breaches preset thresholds, and diversification across carry baskets to reduce single-leg concentration.

Historical example — COVID risk-off (March–April 2020)

During the global dash for dollars at the onset of COVID, the peso sold off sharply: on March 18, 2020, USD/MXN printed a then-record around 24.08 as markets fled EM risk. Banxico responded with an emergency 50 bps rate cut on March 20, 2020, and additional liquidity measures. The selloff extended into late March/April, with USD/MXN pushing above 25.00 at the peak before gradually retracing as conditions stabilized.

Gap risk & policy shocks. Elections, CPI releases, and Banxico/Fed surprises can produce overnight/weekend gaps that slip past stops. Common mitigants include event-driven risk budgets, tracking implied vols/risk-reversals as stress indicators, options overlays (e.g., USD calls/MXN puts), wider catastrophic-gap stops, and lower leverage allocations around major events.

Leverage & margin cascades. High headline leverage (e.g., 1:100) can turn modest adverse moves into margin calls. Typical controls include caps on effective leverage, hard daily/weekly loss limits, and circuit-breaker policies that automatically flatten exposure after a threshold loss.

Liquidity crunch & spread blowouts. Off-hours and holidays tend to widen spreads and increase slippage. Execution policies often prioritize liquid sessions, incorporate US/MX holiday calendars, apply minimum depth/spread filters, and use staggered exits instead of a single market order.

Conclusion

Uncovered interest rate parity is a helpful “zero‑alpha1” benchmark: on average, carry should not produce extra returns. In practice, especially in EMs, a risk premium exists but pays out unevenly and depends strongly on market regimes. Our opportunistic approach is an attempt to marry the carry idea with more flexible exposure management.

Disclaimer. This material is for education only and is not investment advice. Trading FX on margin involves significant risk, including loss of all capital. Past performance (including demo) is not indicative of future results. Live outcomes can differ due to slippage, financing costs, and liquidity constraints.

References

- CARRY TRADES AND RISK by Craig Burnside

- Mexican peso hits all-time low amid coronavirus fears by Reuters

- The Forward Premium Puzzle Revisited by Guy M Meredith,Yue Ma